- Quick Contact:

- +91 22 2167 8100

ECONOMIC BENEFITS OF RECENT LODR AMENDMENT - MMJC

Introduction

Securities and Exchange Board of India (‘SEBI’) vide its third amendment notification dt: 12 December 2024 [LODR Third amendment’] amended SEBI (Listing Obligations and Disclosure Requirements), Regulations, 2015 (‘LODR’).

LODR Third amendment has brought ease for listed companies by modifying, relaxing and integrating some of the provisions of LODR which now appears to be aligned with practical challenges.

One of significant amendment that needs to be highlighted is relating to regulation 42 of LODR which provides for fixing of record date for various corporate actions including dividend.

Background

Let us first understand what are changes in the Regulation 42

| LODR regulation | Prior to LODR Third amendment | LODR Third amendment | Change / Impact |

| Reg. 42(2) | “The listed entity shall give notice in advance of atleast seven working days (excluding the date of intimation and the record date) to stock exchange(s) of record date specifying the purpose of the record date”…. | – | With effect from LODR Third amendment of the time gap between for intimation of record date to stock exchange and record date fixed is reduced to three working days from seven working days earlier. |

| Reg 42(3) | “The listed entity shall recommend or declare all dividend and/or cash bonuses at least five working days (excluding the date of intimation and the record date) before the record date fixed for the purpose.” | Deleted | Earlier listed entities were required to keep the record date for the purpose of dividend only after 5 days (excluding date of intimation and record date) of declaration/recommendation of dividend. |

| Reg 42(4) | The listed entity shall ensure the time gap of at least thirty days between two record dates. | Now the time gap between two record dates is reduced to five working days. |

Impact of the Amendments in Regulation 42 of LODR

Prior to LODR Third amendment listed companies were required to fix a record date post board meeting date as it was necessary to keep a gap of five clear working days between declaration of dividend and record date fixed for dividend. Further, under section 123 of Companies act, 2013, companies are required to transfer dividend to separate bank account within 5 days of declaration. In compliance with this listed entities were required to transfer amount of dividend to a separate bank account within five working days from declaration of dividend.

This required listed companies to keep the amount of dividend idle in a separate bank account for two working days as time gap between declaration of dividend and record date was mandatorily required to be five clear working days. Hence even if companies act required dividend to be transferred to a separate bank account withing five days from the date of declaration of dividend, LODR [reg 42(3)] mandated time fixing record date after a time gap of five clear working days to ascertain amount of dividend payable to shareholders. This mandated listed companies to keep dividend amount lying in a separate bank account for two working days.

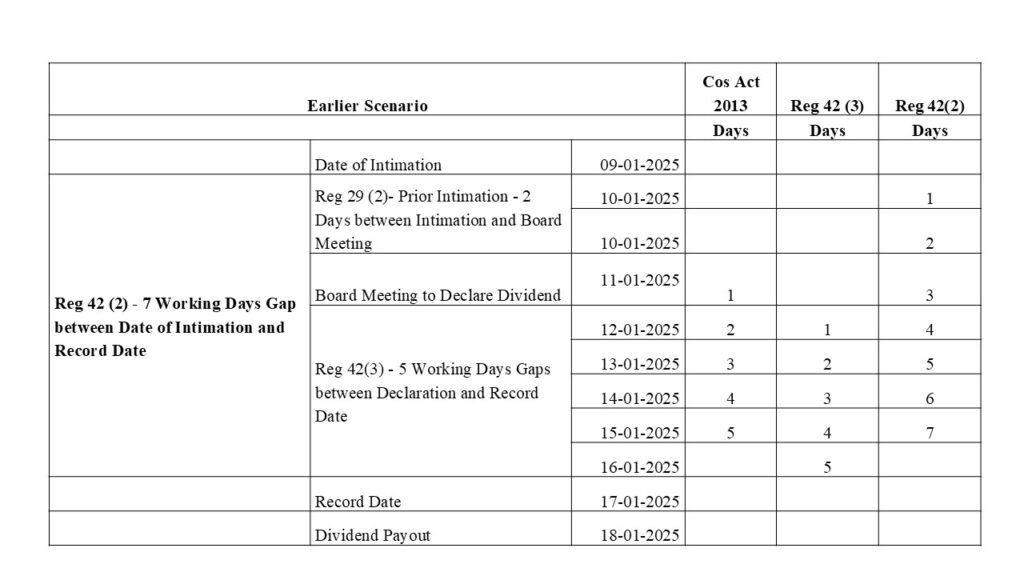

Let’s try to understand by example

In the given Case, Company ABC Ltd is giving prior intimation of 2 days to Stock Exchange on 9 January 2025 under regulation 29, further board meeting is on 11 January 2025, Record date fixed is 17 January 2025.

- Compliance of 42 (2) – 7 Days gap between Date of Intimation and Record Date, i.e. 9 Jan 2025 and 17 January 2025

- Compliance of 42 (3) – 5 Days gap between Recomending dividend and Record Date, i.e. 11 January 2025 and 17 January 2025

- Compliance of Section 123 (4) of Companie Act, 2013 – dividend amount to be transferred by 15 January 2025, i.e. within 5 days from declaration/

- Additional waiting period is 17 January and 18 January.

Now since Regulation 42 (3) is deleted listed companies can keep record date within 5 days of declaration and recommendation or even before the board meeting.

Listed companies having lakhs of shareholders have dividend pay out amount in crores of rupees. Considering this till now dividend amount was required to be kept in separate bank account idle for two days, causing loss of interest/use of funds for any other purpose.

With this amendment now listed companies can transfer the amount of dividend immediately after the record date and disburse the same to shareholders immediately thereafter. This would help companies save the amount of interest, which may be of sizeable amount, considering that dividend amount runs into crores of rupees.