Introduction

In accordance with the powers conferred by Section 454 of the Companies Act, 2013 (the Act), the Central Government, through the Ministry of Corporate Affairs (MCA), designated the Registrar of Companies (ROC) as the adjudicating officer for the purpose of conducting in-house adjudication of non-compliances under various provisions of the Act. In exercise of these powers, the ROC has been issuing adjudication orders and imposing penalties for offences that have been decriminalized under the Act.

This article endeavours to underscore significant orders issued by the Registrars of Companies (ROCs) in India during the financial year 2024-25, while also identifying and examining instances wherein ROCs have adjudicated contraventions of the Companies Act arising from compliance lapses incidental to the ordinary course of business operations of companies. Through an analysis of these instances, valuable insights can be garnered into the prevalent pitfalls and challenges encountered by companies in ensuring adherence to regulatory requirements, thereby emphasizing the imperative of establishing robust compliance frameworks to preclude such lapses.

While this article focuses on adjudication orders passed during the financial year 2024–25, it is important to view these trends in light of recent amendments introduced by the Ministry of Corporate Affairs effective July 2025, involving migration of set of 38 forms (including Annual Filing forms, Audit/Cost Audit Forms) from Version 2 to Version 3 of the MCA portal. This transition introduces more rigorous system-based validations and tighter filing protocols. These improvements are expected to enhance the accuracy and traceability of filings, which in turn may lead to faster detection of non-compliances and data-driven adjudication proceedings in the future.

Statistical overview of adjudication during the financial year 2024-25.

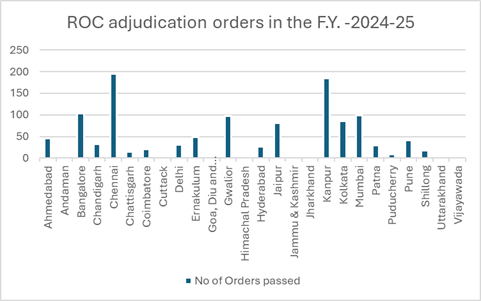

A total of approximately 3600 orders passed by the ROC across the country are available on the MCA portal out of which around 1150 orders were posted in financial year 2024-25. This is about 31% of the total orders passed. Given below is the graphical view of the ROC adjudication orders passed based on the jurisdiction, for the financial year 2024-25

With the commencement of the adjudication process, certain provisions of the Act were adjudicated for the first time and the adjudication orders were made available on the MCA portal during the financial year 2024–25. These include Section 2(68), Section 15, Section 150, and Section 196 of the Act. The details of the orders passed are discussed below:

- Violation of clause (68) of Section 2 of the Act: section 2(68) of the Act provides for definition of private company where private companies were required to maintain minimum paid-up capital of Rs. One Lakh or such higher amount as prescribed by its articles.

In the matter of Reflektion Media Software (India) Private Limited, the company had filed adjudication application for failure to maintain the requirement of minimum paid-up capital during the period 29-11-2012 to 28-05-2015. Penalty was imposed on the company and its officers in default under section 450 of the Act[1].

It is important to note that the requirement of maintaining minimum paid-up capital was omitted by the Companies (Amendment) Act 2015[2] w.e.f.29th May 2015.

An important point of consideration for private companies is that if their Articles of Association (AOA) specify a minimum capital requirement in line with the provisions prior to the Companies (Amendment) Act 2015, and the paid-up share capital falls below that threshold after the amendment, it may constitute a breach of the Articles, even though the statutory requirement has been removed.

- Violation of Section 15(1) pertaining to the requirement of recording alterations in the Memorandum and Articles of Association.

According to Section 15(1): “Every alteration made in the memorandum or articles of a company shall be noted in every copy of the memorandum or articles, as the case may be.”

In the matter of Feranbraj Toll and Highway Private Limited, during the examination of Form MGT-14, it was observed that the company failed to note the alterations made in the copies of the Memorandum and Articles of Association as required under the above provision. Penalty was imposed on the company and its officers in default, under Section 15(2) of the Companies Act, 2013[3].

- Violation of Section 150(1) outlines the requirements for the selection of independent directors and the maintenance of the independent directors’ databank.

As per Section 150(1) read with Rule 6(1) of the Companies (Appointment and Qualification of Directors) Rules, 2014, an individual to be appointed as an independent director must have their name registered in the independent director databank prior to their appointment.

In the case of Banswara Syntex Limited, it was observed during the examination of MGT-7 filed for the FY 2023-24 that the company had appointed an independent director. However, the appointed individual’s name had not been registered in the Independent Directors Data Bank at the time of appointment, in violation of Section 150(1) read with Rule 6(1) of the Companies (Appointment and Qualification of Directors) Rules, 2014.

Although the company rectified the lapse later, a penalty was imposed under Section 172 on both the company and its officers for the period of default[4].It outlines the importance of verifying the registration of the proposed independent director in databank beforehand to avoid such instances, as companies may have stringent timelines to meet the minimum requirement of composition of Board and the committees as applicable.

- Violation Section 196 governs the appointment of Managing Director, Whole-time Director, or Manager.

Subject to the provisions of Section 197 and Schedule V of the Companies Act, the appointment of a Managing Director, Whole-time Director, or Manager, along with the terms and conditions of such appointment and the remuneration payable, must be approved by the Board of Directors at a duly convened meeting. This approval is further subject to confirmation by a resolution passed at the next general meeting of the company. Additionally, if the appointment deviates from the conditions specified in Part I of Schedule V, it must also be approved by the Central Government.

In the case of SML Isuzu Limited, the company filed an application seeking Central Government approval under Section 196 read with sub-clause (e) of Part I of Schedule V for the re-appointment of a Whole-time Director (who was a foreign national) for a period of one year. On examination of the application and the company’s response to the queries, it was observed that no approval was sought for the previous appointment of the same individual as Whole-time Director. Apparently, it was observed that in the 12 months period before his appointment, the appointee had remained out of India for 57 days, which supposedly triggered the requirement of Central Government approval as per the provisions.

As the company did not seek approval of Central Government for the previous period of appointment, penalty was imposed on the company and its officers in default under Section 450 of the Act for contravention of the provisions[5]. One notable factor to be considered at the time of appointment of managing director or whole-time director or a manager is to verify residential status as per the explanation provided in Part I of schedule V and seek the necessary approval wherever required.

Examination of additional key sections under which adjudication orders were issued

Let’s examine some more adjudication orders issued by ROCs for breaches under the Companies Act that occurred during the normal course of a company’s business operations and that warrant focused attention due to repeated instances of non-compliance. :

Section 12-Registered Office of Company.

This is a key compliance area often missed, under which the ROC has issued numerous adjudication orders for reasons like, failure to maintain registered office, failure to intimate change in registered office, failure to mention CIN No. on the letterhead and other documents, failure to mention address of the registered office in which its business is carried on in the language in general use in that locality. These lapses were identified when physical verification of registered office was ordered or when any communication made at the registered office was returned undelivered for which penalty was imposed under section 12(8). During the financial year 2024-25 around 175 orders were passed under this section.

Section 155- Prohibition to Obtain More than One Director Identification Number.

It was observed that the directors had filed suo-motu applications for holding more than one DIN, resulting into violation of section 155 of the Act for which penalty was imposed under section 159. During the financial year 2024-25 around 8 orders were passed under this section.

Section 29- Public Offer of Securities to be in Dematerialised Form read with Rule 9A of the Companies (Prospectus and Allotment of Securities) Rules, 2014

Here the major compliances that were missed were failure to convert their physical shares in dematerialized form, transfer of shares executed in physical form for which penalty was imposed under section 450. During the financial year 2024-25 around 10 orders were passed under this section.

Section 42- Offer or invitation for subscription of securities on private placement

The Registrar has also been issuing orders under section 42 for non-compliances namely:

- Fresh offer for shares without completing the process of allotment of shares offered previously as per section 42(5)[6] .

- Failure to keep the funds received on application in a separate bank in a scheduled bank account as specified in section 42(6)[7].

- Delay in filing of PAS-3 as required under section 42(8)[8].

- Utilization of funds before filing of return of allotment as per section 42(4)[9].

- Using media, distribution channel or agent to inform public at large about such an issue as specified in section 42(7)[10].

During the financial year 2024-25 around 10 orders were passed under this section.

Section 56- Transfer and Transmission of Securities

The ROC issued order under section 56 for failure to issue share certificates within the prescribed timeline specified under section 56(4)(a), (b). The ROC imposed penalty under section 56(6). During the financial year 2024-25 around 5 orders were passed under this section.

Section 62- Further Issue of Share Capital

Some of the non-compliances observed under Section 62 include:

- Not passing a special resolution under Section 62(3) prior to raising loans, convertible into shares but converting loan into shares without following the process under section 62(1)(c).[11].

- Failure to make an offer under Section 62(1)(a) to existing equity shareholders at the time of the offer[12].

- Keeping the offer open for more than 30 days, resulting in a violation of Section 62(1)(a)(i)[13].

During the financial year 2024-25 around 11 orders were passed under this section.

Section 89 – Declaration in respect of beneficial interest in any share

In case of section of section 89 of the Act companies failed to intimate changes in beneficial owner of shares or filing of the same in Form MGT-6, within prescribed time for which penalty has been levied under section 89(5) and 89(7).

During the financial year 2024-25 around 18 orders were passed under this section.

Section 90 – Register of significant beneficial owners in a company

The ROC has been vigilant over the identification of significant beneficial owner in the company as around eighty orders were passed by the ROC under section 90 for reason like non- filing/delay in filing of BEN-2, failure on part of company to take steps to identify SBO and send notice in form BEN-4. This shows that Registrar is strictly checking if the significant owner is identified and reported. During the financial year 2024-25 around 83 orders were passed under this section.

One of the important order passed during the year was in case of Linkedin Technology Information Private Limited[14], the details of penalty imposed are given below.

- ROC has imposed penalty for failure to submit accurate declarations in reporting of registered owner under section 89(1) and beneficial owner under section 89(2) for which penalty was imposed under section 89(5).

- Further the ROC also imposed penalty under section 90(10) on the significant beneficial owners for failure to report as per the requirement under section 90(1).

- The company and officers in default were also penalized under Section 90(11) for failing to take the necessary steps to identify the Significant Beneficial Owner, as mandated under Section 90(4A), and further penalized under Section 450 for its failure to issue notice as required under Section 90(5).

Section 172- Punishment

Section 172 imposes penalty for non-compliance with Chapter XI – Appointment and Qualifications of Directors

The Registrar of Companies (ROC) also levied penalties under Section 172 for non-compliance with the following provisions:

- Section 158: Failure to mention the Director Identification Number (DIN) in returns, information, or particulars required to be furnished under the Act.

- Section 149(4): Failure to comply with the minimum requirement of Independent Directors.

- Section 149(1): Non-appointment of a Woman Director, where applicable.

During the financial year 2024-25 around 45 orders were passed under this section.

These instances reflect the importance of adhering to board composition norms and disclosure requirements under the Companies Act, 2013.

Section 134 – Financial Statements, Board’s Report, etc.

The ROC has levied penalty under section 134(8) for non-compliances of

- 134(1)-Financial statements not signed by the Directors of the Company[15].

- 134(2)-Failure to attach auditors report to financial statement[16]

- 134(3)-Matters to be included in the report by the Board of Directors.

- 134(5)- it was found that the company’s Directors’ Report for the year ended 31.03.2017 claimed compliance with applicable Accounting Standards. However, the financial statements revealed non-compliance with AS-15, AS-18, AS-20, and AS-22, with no explanation provided for these material departures. [17].

Around 55 orders were passed during the financial year 2024-25 under this section, orders passed under section 134(3) were on a higher side.

Section 92 – Annual Return

- 92(3) Failure to place extract of annual return on the website.

- 92(4) Failure/delay in filing annual return within time prescribed under the section.

The ROC has levied penalty under section 92(5) for non-compliance of section 92(4) and under 450 for non-compliance of section 92(3).

Section 137 – Copy of Financial Statement to be Filed with Registrar

- 137(1)- Delay/Failure in filing of filing financial statements as required under section 137(1) for which penalty was imposed under section 137(7).

Around 225 orders were passed for non-compliance of section 92 and 137 during the financial year 2024-25.

Section 135 – Corporate Social Responsibility (CSR)

- Failure to spend CSR amount and then transfer the unspent CSR amount to the Schedule VII within six months of the expiry of the financial year as per requirement of section 135(5). Penalty was imposed under section 135(7).[18]

- Failure to constitute CSR Committee as required under section 135(1)

Around 22 orders were passed during the financial year 2024-25 under this section.

Section 179 – Powers of the Board

- Companies missed out seeking boards’ approval for the items listed in sub section 3 of section 179 for which penalty was imposed under section 450, Further these resolutions are required to be filed as per the requirement of section 117(1) with the registrar for which penalty was imposed under section 117(2).

- In case of Ultraviollete Automotive Private Limited, the company appointed wholetime company secretary by passing circular resolution. As per section 179(3) the board can exercise such powers only by means of resolution passed at a duly convened meeting. Penalty was imposed under section 450.[19]

Around 13 orders were passed during the financial year 2024-25 under this section.

Section 203 – Appointment of Key Managerial Personnel (KMP)

- Failure to appoint whole-time key managerial personnel as required under section 203(1) read with Rule 8 and 8A of the Companies (Appointment and Remuneration of Managerial Personnel) Rules, 2014 for which penalty was imposed under section 203(5).

- In the case of Jana Holdings Limited, the company listed its privately placed Non-Convertible Debentures (NCDs) on the Bombay Stock Exchange, thereby classifying it as a “listed company” under Section 2(52) of the Companies Act, triggering compliance requirements under Section 203 where penalty was imposed under section 203(5). The non-compliance in question relates to the year 2017[20].

- It is noteworthy that a proviso was introduced to Section 2(52) of the Companies Act through the Companies (Amendment) Act, 2020, effective from 22nd January 2021. Additionally, Rule 2A of the Companies (Specification of Definitions Details) Second Amendment Rules, 2021, came into force on 1st April 2021. These amendments clarify that certain classes of companies—particularly those issuing privately placed non-convertible debentures (NCDs)—shall not be classified as listed companies.

Around 40 orders were passed during the financial year 2024-25 under this section.

Preventive Mechanism

- The Registrar of Companies (ROC) has taken a stricter stance on enforcing compliance with the Companies Act, 2013.

- Non-compliance not only leads to financial penalties but also to reputational damage for companies.

- To mitigate these risks, companies should:

- Establish strong compliance frameworks

- Engage qualified professionals to oversee compliance activities

- While secretarial audits may not be mandatory for all, companies can enhance governance by:

- Implementing internal review processes

- Adopt maker-checker mechanisms

- With the advent of the MCA Version 3 filing system, companies are now operating in an environment where technology plays an active role in flagging inconsistencies and enforcing timelines. Filings are becoming increasingly traceable, interlinked, and less tolerant to delay or deviation. In such a framework, enforcement may no longer be triggered only by inspection or complaint, but by systemic detection of gaps.

Conclusion

The purpose of gaining insight of the adjudication platform was to understand the implications of compliance failures or shortfalls and to emphasize on the proactive measures companies should adopt to prevent such lapses. Maintaining strong compliance practices enables companies and their officers to avoid unnecessary penalties, thereby allowing resources to be effectively directed toward core business operations

[1] Reflektion Media Software (India) Private Limited- ROC Bangalore Order dated 24th May 2024

[2] The Companies (Amendment) Act, 2015 Notification dated 26th May 2015 w.e.f. 29th May 2015.

[3] Feranbraj Toll and Highway Private Limited -ROC Madhya Pradesh order dated 08th September 2021

[4] Banswara Syntex Limited-ROC Jaipur order dated 23rd July 2024

[5] SML Isuzu Limited-ROC Punjab and Chandigarh order dated 21ST August 2024

[6] Ambium Finserve Private Limited – ROC Punjab and Chandigarh order dated 27th May 2024

[7] Galaxeye Space Solutions Private Limited – ROC Chennai order dated 24th September 2024

[8] Acceler Edtech Private Limited – ROC Pune order dated 30th December 2024

[9] Quadrant Future Tek Limited-ROC Punjab and Chandigarh order dated 08th August 2024

[10] Yotta Agroventures Private Limited, ROC Jaipur order dated 03rd June 2024

[11] Lalitbagh Heritage Palace and Museum Private Limited -ROC Jaipur – order dated 08th May 2024

[12] Longcheng Composites Private Limited – ROC Pune – order dated 28th May 2024

[13] Kanishk Aluminium India Private Limited -ROC Jaipur – order dated 14th August 2024

[14] Linkedin Technology Information Private Limited – ROC Delhi & Haryana – order dated 22nd May 2024

[15] Apsal Chits Private Limited – ROC Chennai – order dated 24th September 2024

[16] Meghana Homes Private Limited – ROC Bangalore – order dated 26th November 2024

[17] Pasari Exports Limited – ROC Bangalore – order dated 26th November 2024

[18] Ingeteam India Private Limited – ROC Chennai order dated 03rd October 2024

[19] Ultraviolette Automotive Private Limited – ROC Bangalore – order dated 28th November 2024.

[20] Jana Holdings Limited – ROC Bangalore – order dated 04th December 2024

This article is published on taxmann link below.